I’ll be running an occasional series of financial Q&As. These are curated questions I’ve answered in other financial forums. I may edit for clarity and change details to preserve privacy. Remember, I am not a financial professional so this is for your entertainment only. If you’d like to as a question, please reach out to me through this blog.

Q: I recently got a chunk of money from the sale of my house. I plan on continuing to rent for the near- to mid-term so I want to invest this money. I’m afraid to dump it into the market though because it is currently at an all-time high. What should I do?

A: Ahhh, this is a very common question. There is a real emotional component to investing and a lot of people struggle with loss aversion at the idea of their hard earned money suddenly dropping in value right after it gets invested. As a result of this fear people can drag their feet on investing as they wait for “the dip” (“I’ll invest after the market corrects”). The result of waiting is usually that they miss out on the continued upward rise of the stock market while their money sits on the sidelines in cash, slowly being eroded by inflation.

Is the solution just to hold your nose and jump into the deep end of the pool? In a word, yes. However it is a lot easier to jump in if you understand what is going on so it isn’t so scary.

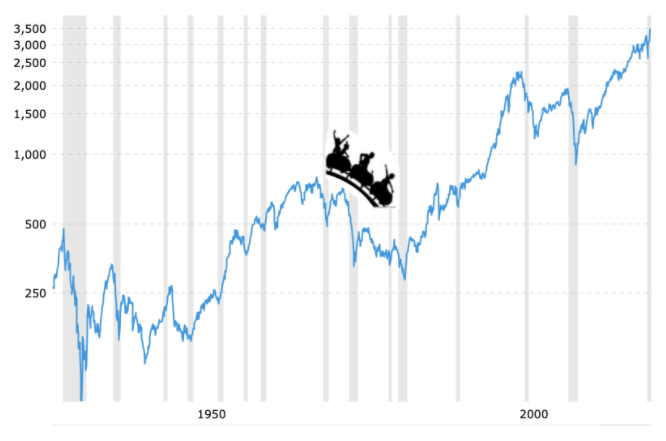

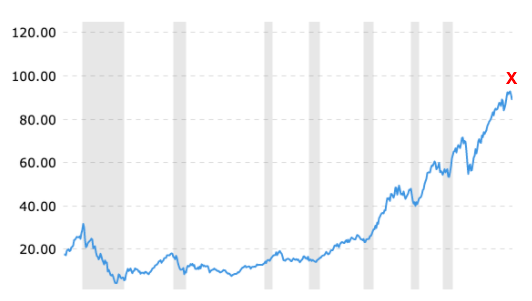

Have a look at this snapshot of several decades of the S&P 500 index. It is a bit of a wild ride. You can see how someone sitting where the X is debating whether to invest or not could reasonably say “I’m not sure about dumping my money in there since we are at an all-time high”. That person is correct, the market is at an all time high!

I purposefully didn’t include the dates so you can’t guess what will happen next because real life investing is like that. Unless of course you have a crystal ball, in which case please send me a PM so we can chat. 🙂

Our hypothetical investor is in it for the long haul – perhaps this is retirement money we are talking about, so fluctuations over months or even years are okay in the long run. The question is then: should our investor jump into the cold, cold water of the deep end of the pool or perhaps wait for a dip or dollar cost average the money in over time? Let’s look at each of these in turn.

Wait For a Dip: Market Timing

Market timing is playing the game of watching the stock market fluctuate up and down while trying to time an entry (i.e. choosing when to invest) such that you buy when prices are lower. The hope is to buy low and then watch your investment go up and avoid buying high and watching your investment go down in the short term. Market timing can also be selling everything when you think the market will go down in hopes of avoiding a paper loss with the plan of re-entering the market at some unspecified future date.

Vanguard has done a study simulating what happens when an investor takes his or her money out of the market for various time periods ranging from 1 to 240 days in hopes of avoiding the worst days. This simulation showed that the average investor underperformed the market in every case. The more consecutive days the average investor is out of the market, the more the investor underperforms the market.

But what about the extraordinary investor? I suspect that most people who try to time the market feel deep down inside of them that they are smarter than the average bear. Well, even the most extraordinary of investors, the top 1%, underperformed once they were out of the market for more than 135 consecutive days. In the best of cases with our 1% investor being out of the market around 35 consecutive days a year, the performance premium was around 1.8% over the market return. Ask yourself: is an additional 1.8% return a year worth correctly guessing when to get in and out of the market each year? That requires a lot of guesswork and/or luck as evidenced by the fact that 99 out of 100 people wouldn’t be able to achieve that. (Side note: you can play a game to determine how awesome of a market timer you really are here.)

Why is this? It helps me to think about the long term trend of the stock market. Thinking back to our investor wondering whether to invest or not, let’s zoom out and see what happens over time.

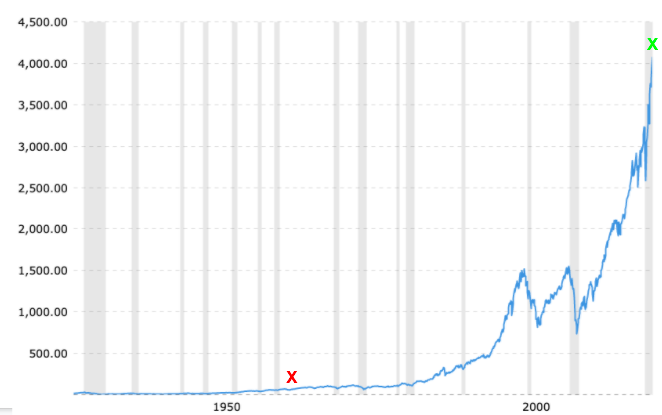

S&P 500 index over time, 1927 – present, inflation adjusted

With the benefit of hindsight (or a crystal ball) the previously intimidating question of whether to invest or not at the red X seems insignificant compared to what the market did over the following decades. Yes, the ride was sometimes boring, sometimes too exciting, but the buy-and-hold investor would be remarkably well compensated for holding tight over the long run. The reason for this of course is that on average, over time the stock market goes up. Up, up, up. So the more time you spend invested in the market, the more time your money has to go up, up, up.

Dollar Cost Averaging: Spreading Your Bets Out (Or Just Delaying the Risk)

Dollar cost averaging is a process by which an investor breaks up a sum of money into several portions that are then invested periodically over a set period of time. For example, an investor may decide to invest $10,000 in $1000 increments over 10 months instead of sticking it all in the market at once. This is similar to when you invest in your 401(k) or IRA each month when your paycheck hits, though technically that is periodic investing and not lump sum investing, as you are investing the money as soon as you get it (payday). When you invest each pay period you buy at market highs and market lows and everything in between. With your 401(k) you always invest your money as soon as you have it; with dollar cost averaging a portion of your money stays in cash while a portion of it is invested at regular intervals.

Our trusty Vanguard has come out with another study where they investigated the differences between lump sum and dollar cost averaging (DCA). The study varied the time over which DCA was performed, the portfolio asset allocation, and even the country the investing was done in and found that overall lump sum investing produced larger ending portfolios in 67% of the cases. The reason for this is the same as above: on average, the market goes up more than it goes down, so on average, you will end up with more money if you are invested as soon as possible over keeping your money in cash.

Pulling It All Together

The math is pretty clear: on average, you are better off dumping all of your money into the market immediately. Investing is never purely about math however. There is an emotional component that may be difficult to swallow. Two thirds of the time lump sum investing is the winning strategy, but what happens if you get unlucky and invest in one of the 33% of the times when the market goes down after you invest? If you panic and sell low, then it doesn’t matter what the math says because you just shot yourself and your portfolio in the foot.

The most important thing in investing is to stick to your plan. If breaking an investment into chunks and investing incrementally will help you sleep well at night, then go for it. Just be aware of the tradeoffs and try to keep the period over which the dollar cost averaging takes place as short as possible.