Often I will see someone new to investing talk about being scared to invest in “risky” things like the stock market. When the world of investing seems wild and unknown there can be a psychological preference for “safe” investments like CDs or bonds, or something that is easier to intuitively understand, like real estate. The use of terms like “risky” and “safe” in the context of investments is one of my pet peeves, so I’d like to break this down and encourage us to use better language to describe these commons terms in personal finance.

In the world of personal finance and investing there are two most common risks that get discussed often: volatility and inflation. Volatility is a short-term risk, and describes how an investment can fluctuate in price over a short time period. Think of a roller coaster going up and down, sometimes at breathtaking speeds.

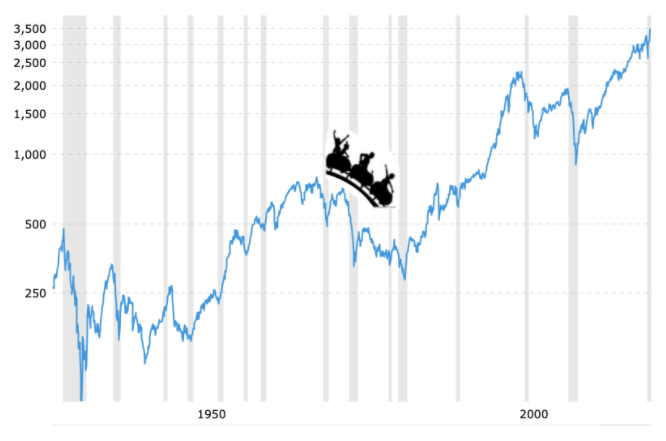

S&P 500 Index – 1927 to present (source)

The S&P 500 is a stock market index tracking the 500 largest publicly-traded firms in the US as measured by market capitalization. As you can see from the graph above, the price of this basket of stocks is pretty volatile, meaning the price fluctuates quite a bit over time. Sometimes the price squiggles just a little bit and sometimes it takes some deep dips, erasing years of previous gains in a short period of time.

Inflation is the idea that over time a dollar is worth less and less because the cost of goods slowly rises.

Often when inflation is discussed as a risk people implicitly mean hyper inflation, like present-day Venezuela or Germany after WWI**. While wheelbarrows full of bills used to buy bread is a dramatic example, inflation under normal conditions is much subtler and only shows its force over time.

Inflation in the US varies over time, but over the past 4 decades or so it has hovered around 3%. The Fed currently has a target inflation rate of 2% consistent with their target of strong employment and price stability. These are nice, low numbers, but keep in mind that any time your money earns less than inflation, it is like a little mouse nibbling away at the edge of your cookie; those bites are small but if you let it go on for long enough you will soon find yourself with little cookie left.

What this means for investing and retirement

Before her death my grandmother had her nest egg in CDs. She felt comfortable with this nice, “safe” investment. She likely remembered being retired in the early 1980s when CDs were paying 10-12%. The problem with her “safe” investment is that every year she was losing ground.

Turning to my favorite portfolio simulation tool cFIREsim.com I modeled what my grandmother’s retirement spending might have looked like. I assume she retired with a nest egg of $500,000 and spent $20,000 a year, adjusted upwards for inflation. We’ll run this simulation for a 30-year retirement.

| Starting portfolio | $500,000 | ||

| Yearly Spending | $20,000 | ||

| “Safe”: 50% bonds / 50% cash | Balanced: 50% stocks / 50% bonds | “Risky”: 100% stocks | |

| Portfolio success rate | 46 | 93% | 95 |

| Average ending portfolio value | $197,757 | $654,456 | $1,530,860 |

| *Assumes 5% average growth of cash |

Nest egg performance of “safe” and “risky” portfolios

I find the results super interesting so let’s notice a few things:

- The “safe” (i.e. low volatility) portfolio composed of half cash and half bonds fails over half of the time and on average leaves you with less than half of what you retired with.

- A wildly inappropriate “risky” portfolio of all stocks is successful 95% of the time and leaves you with three times as much money as you retired with, on average.

- A balanced portfolio, so called for being half stocks and half bonds, has pretty much the same solid success rate as our crazy all-stock portfolio. Having those bonds smooths out the wild fluctuations of an all-stock portfolio but we pay for it by not being nearly so rich at death.

Conclusions

Looking at these results you can see why I cringe when I hear portfolios heavy in bonds and cash dubbed “safe” and stock-heavy portfolios referred to as “risky”. In the short term volatility is risky and inflation doesn’t really matter. However in the long term volatility hardly matters at all but inflation is the biggest risk to your portfolio. We need to be more precise when identifying what risk we are talking about.

If you need your money soon, say for a down payment, then you can’t tolerate the volatility of the stock market and so keeping your money in cash is indeed “safe”. However when investing for the long term like your retirement, “safe” investments that don’t outpace inflation are one of the riskiest things you can be in. That is why I always use “high volatility” and “low volatility” to describe investments, or otherwise make sure to specify what risk I am referring to. I encourage you to do the same.

**Side note: I spent a summer in Russia in 1997 when the exchange rate was around 5,700 Ruble to the dollar. I remember pocketing a 100,000 Ruble note when heading out for a night of dancing and drinks at the discotheque. Soon after I went home Russia cut three zeros off the Ruble and issued new currency.